March CPI Is Peak Inflation

I’m ready to go toe to toe with Jeff Gundlach, the purveyor of 10% inflation. Everyone saw today’s March CPI report from the BLS, where inflation came in at a whopping 8.5% (which is askew for obvious reasons, but we won’t get into that here). The most important thing is that we’ve weathered the inflation storm at this point, and we’re off to much greener pastures.

And that is ostensibly true according to major names such as Goldman, J.P. Morgan, and Deutsche. While Goldman’s revised GDP forecast for 2022 was arguably the most embarrassing macro take that has come into existence this year, I will side with them as it pertains to the inflation narrative. Nicely done, Ligma Sachs (shoutout Litquidity).

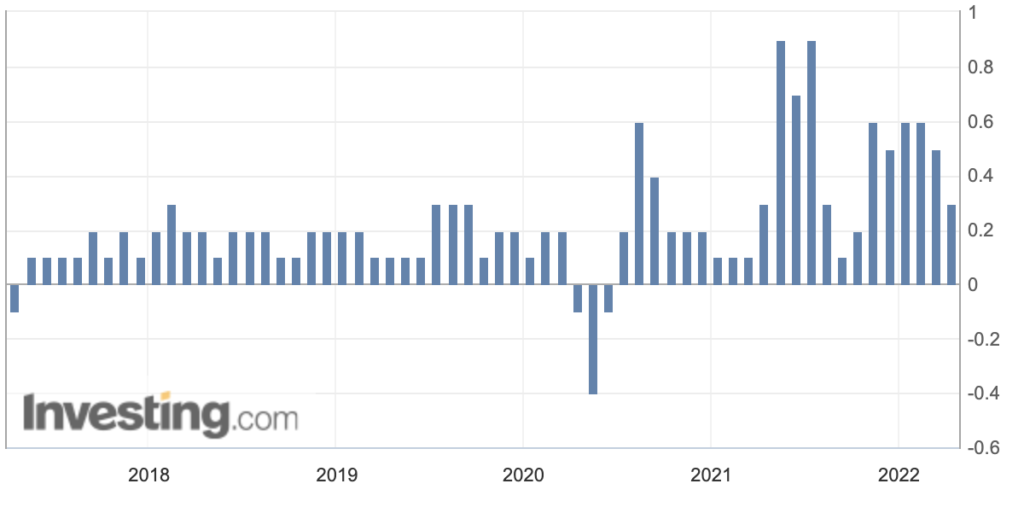

First things first, Core CPI, MoM came in at 0.3%, missing expectations of 0.5%. This rise is at the slowest level since September 2021, suggesting a gradual downturn in comings months.

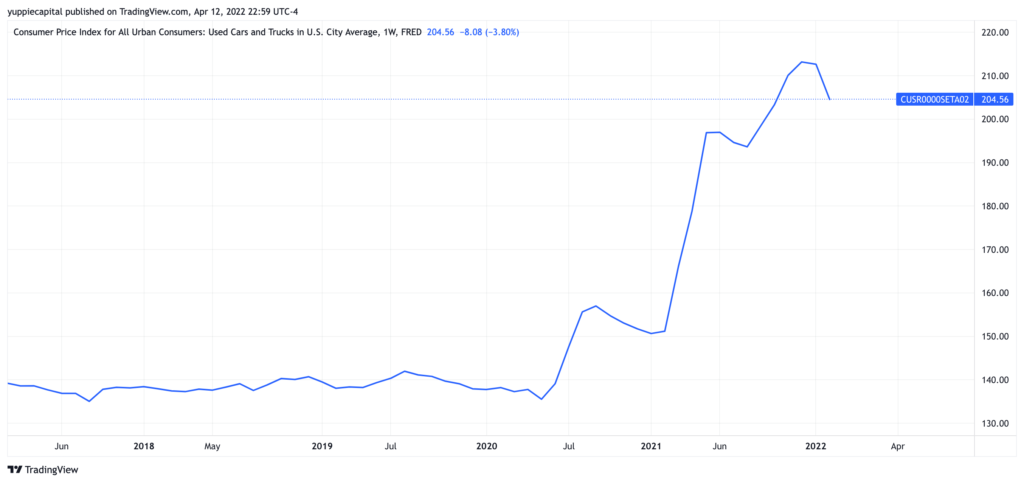

The largest contributor here (and was the most obvious macro prediction), was used cars. I will give Jack Bouroudjian credit here because he called this back in December, even before we started to see absolutely runaway inflation. Anyways, the BLS reported today that the used cars and trucks index fell 3.8% this month, marking the second straight monthly decline.

The funniest part of this all, is that the metric as to the weighting of used car prices will change according to the BLS. I didn’t even want to cover housing inflation data, because it’s arguably the most disingenuous data set representation known to mankind. For anyone who is interested, just Google “Owner’s Equivalent Rent” and all your questions will be answered (although you’ll probably be left with more upon reading). In any case, our good buddy Michael Burry (the guy who saw the looming housing bubble in ’08), pointed out an excerpt from the BLS which unveils their plans to wallop used car prices and drive the CPI down even more so.

Even amidst the arguable worst of the Russia & Ukraine fiasco, we’ve seen oil prices level off as of recent.

Strategic outflows of oil reserves have also helped ease the strain on the oil market, and have helped calm rising oil prices in the face of just absolute carnage unfolding within Ukraine. It’s likely that oil will continue to remain steady, and also trend lower, amidst decreased consumer outlook and a bleak macro forecast from many chief economists. As I’ve said before, the U.S. is facing just about every economic headwind known to man. With not only oil trending lower in the month of April (and in the coming months), we’ll begin to see the aforementioned macro effects at play which will ultimately drag CPI lower from its peak in March. Book it, baby.

I wonder what Peter Schiff’s prediction is, though?