That Shit Hurted

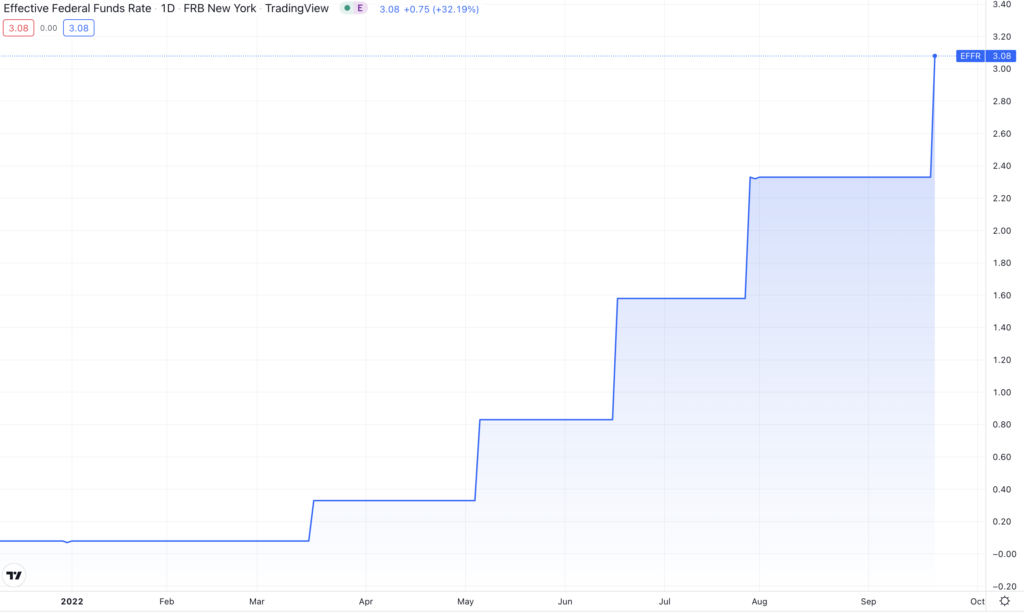

Yikes. Where do we even start? I guess Fed Chairman Jerome Powell really started the party this week by solidifying a 75bps rate hike, which sent equities into an absolute frenzy, and the sell-off continued throughout the remainder of the week. During Friday’s trading day, indexes broke down the June lows on an intra-day basis, but finished the day just above those lows, but still in bear market territory. “Ring of FIre” by Johnny Cash seems incredibly fitting at the moment.

To think that equities/commodities are prepared for the economic shitstorm that is about to ensue is nothing short of an understatement.

First off, we are on track for the fastest 6 month increase of interest rates since 1981. We are stopping businesses dead in their tracks right now as companies across the board will begin to slow debt financing, which will eventually hinder their growth (bottom line gets rekt). Most financial strategists suggest that the Fed was quite literally “asleep at the wheel” when it came to letting inflation run rampant, which is completely accurate. However, it was truly awesome to be a part of the most epic bull run in virtually every asset class during the roaring twenties liquidity hype train extravaganza.

Secondly, the U.S. Dollar has had the most immaculate bull run of all time, and actually reached an ATH during Friday’s trading day.

While a stronger U.S. Dollar is good for domestic consumers and foreign exporters, it’s not great for U.S. corporations. In addition to the diminishing liquidity and deteriorating credit conditions, a strong U.S. Dollar is just the poop-flavored icing on the cake of recessionary headwinds that we are in the middle (or early stages) of weathering.

It’s also worth noting that Goldman cut their 2022 forecast for the S&P 500 (similar to their revised GDP forecast earlier this year). Treasury yields (AND REAL YIELDS) were ripping this week, economic activity within Europe is slowing to a grinding halt, and everyone is collectively pissing their pants (including myself).

Where does this end? There is only one way.